PMBOK divides Project Cost management into four sequenced processes which involve planning, estimating, budgeting, financing, funding, managing, and controlling.

Those processes are:

Plan Cost Management

Estimate Cost Management

Determine Budget

Control Cost

Step 1: Plan Cost Management

Overview

According to PMBOK this is the mechanism of outlining how project costs will be estimated, budgeted, managed, monitored and controlled. It occurs early in the project planning process and establishes a basis for each cost management element ensuring efficiency and coordination. It is an activity which can be performed at a single time or at pre-defined points throughout a project. The Cost Management Plan is the Output of this Process.

Below are the inputs, tools and techniques and outputs of the Plan Cost Management process.

Inputs

Key Inputs are the Project Charter, the Project Management Plan specifically the Schedule Management Plan and Risk Management Plan. Enterprise Environmental Factors and Organisation Process Assets are also inputs to this process.

The Project Charter is the source of pre-approved financial resources and defines approval requirements

The Schedule and Risk Management Plans provide processes and controls that effect cost estimation and management

Examples of Enterprise Environmental Factors include; organisational culture and structure, market conditions, currency exchange rates, published commercial information, project management information system, productivity differences globally

Examples of Organisational Process Assets include; financial controls procedures, historical information, lessons learned repository, financial databases, existing formal and informal cost estimating procedures

Tools and Techniques

Amongst the tools and techniques recommended for cost management planning are Expert Judgement, Data Analytics such as Alternative Analysis and Cost Management Planning Meetings.

Expert Judgement should be sought from individuals or groups with knowledge of the following; previous similar project, information in the industry/discipline/application area, cost estimating and budgeting, earned value management

Alternative Analysis (see Figure 2) may include review of strategic funding options (e.g. self-funding, funding with equity, funding with debt) and ways of acquiring project resource (e.g. making, purchasing, renting, leasing)

Recommended attendees for Cost Management Planning meetings include the project manager, project sponsor, selected team members and stakeholders, personnel with responsibility for project costs, others as required

Outputs

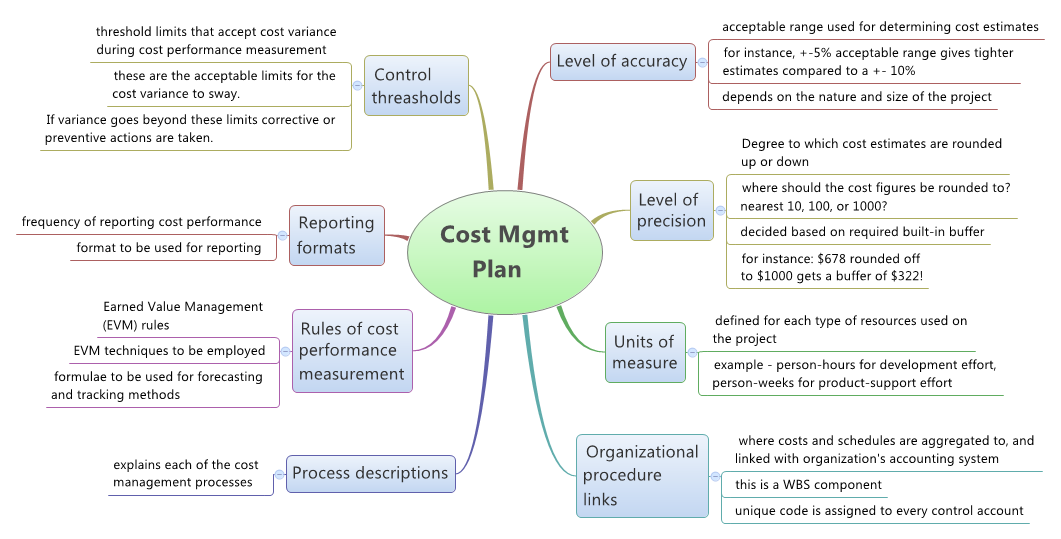

The output of this process is the Cost Management Plan (see Figure 1 above).

The Cost Management Plan outlines how the project costs will be planned, structured and controlled

It may establish: Units of Measure, Level of Precision, Level of Accuracy, Organisational Procedure links, Control Thresholds, Performance Measurement Rules, Reporting Formats and Additional Details as required

Step 2: Estimate Costs

Overview

The process of estimate costs is based on the approximation of the costs of resources required to complete the project. The monetary resources required are also determined in this process. It is an iterative process and a quantitative assessment of the likely costs of the resources usually expressed in units of some currency. It can be reviewed and refined throughout the project.

The estimates start with Rough order of Magnitude (ROM) in the range of -25% to 75% and as more information is known in the project, the range of estimates is narrowed to -5% to 10%.

Estimate Cost Process:

Inputs

Inputs to the Estimate costs process are pretty much the same as the inputs of the plan cost management process with the exception of the Project Charter which is not an input for estimating costs. Project documents such as Lessons learned register, project schedule, resource requirements, and Risk Register are also used as inputs to Estimate Costs.

Tools and Techniques

Expert Judgment is a common technique that is used for almost all processes. In this case, the expert should have

specialized knowledge or training in similar projects, information on the industry, discipline, and application area, and cost estimating methods.

Others specific techniques can be used for estimating costs such as:

Analogous estimating – values and attributes such as scope, cost, budget, duration, etc of previous projects are compared and estimated in the same parameter or measurement for the actual project.

Parametric estimating – considers the statistical relationship between relevant historical data and other variables.

Bottom-up estimating – estimate a component of work to the greatest level of specified detail.

Three-point estimating- range for activity costs are determined by most likely (cM), optimistic (cO), and pessimistic (cP).

Triangular distribution: cE = (cO+cM+cP)/3

Beta distribution: cE = (cO+4cM+cP)/6

Data analysis techniques that can be used to estimate costs:

Alternative analysis – choose between options.

Reserve analysis – Contingency reserves to address the known-unknows.

Cost of quality – additional investments in conformance versus nonconformance.

Project Management Information System (PMIS) – such as spreadsheets, simulation software, and statistical analysis tools and, Decision making – outcome from multiples alternatives by voting.

Outputs

There are three outputs of this process which are:

Cost Estimates – can be in summary form or in detail of quantitative assessments, contingency amounts for identified risks, and management reserve to plan unplanned work.

Basis of Estimates – detailed information on how costs estimate was derived by application area.

Project documents updates such as Assumption log, Lessons learned register and, risk Register.

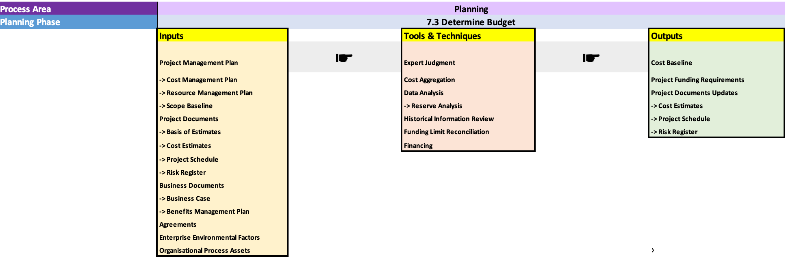

Step 3: Determine Budget

Another aspect of cost management is determining the budget, which according to PMBOK involves aggregating the various estimated costs involved in the project. This allows a cost baseline to be created to allow comparison of project costs at various stages throughout the project.

Traditional project management approaches such as PMBOK look at multiple inputs, tools, techniques and outputs when determining the project budget.

Inputs

The inputs to this process are the project management plan (which includes documents such as the cost management plan, resource management plan and scope baseline), project documents (including basis of estimates ,project schedule, cost estimates and risk register), business documents (such as the business case and benefits management plan), any agreements or contracts involved in the project and enterprise environmental factors and organisational process assets, all of which are required to determine the budget.

Tools and Techniques

There are many different tools and techniques that can be used to determine the budget and ensure it is as accurate as possible. One of these is the use of expert judgement, which involves gaining information from those with experience on similar projects, or those with specialised knowledge or training. Another tool that can be used to ensure accurate budgeting is cost aggregation. This process involves looking at the individual work packages that make up the project and combining all the cost estimates of each one to get the final cost estimate.

Reviewing historical information can also help in determining the budget on a project. These can involve looking at various mathematical or statistical models to determine the full project costs and budget. However, the accuracy of these models is determined by the information used when forming the model being accurate. It is also important that the model can maintain accuracy for smaller and larger projects, or at least being aware of its limitations in terms of scalability.

When determining the budget, it is also important to look at any limits on funding commitments. Any variances between funding limits and planned expenditure should be highlighted and according to PMBOK(2) can be dealt with by looking at bringing in date constraints to the project. As well as limits on funding, certain external funding may have certain dependencies or requirements which should also be taken into account.

Outputs

Therefore the outputs of this process are;

Cost Baseline

Project funding requirements

Project document updates

Cost estimates

Project schedule

Risk register

Step 4: Control Costs

Overview

According to PMBOK (2017), Control Costs is “the process of monitoring the status of the project to update the project costs and managing changes to the cost baseline”. This is critical to ensure that the cost baseline is maintained through the project.

Inputs

Key Inputs are Project Documents, the Project Management Plan, Project Funding Requirements and Organisational Process Assets.

Project Documents would include the Lessons Learned register.

Project Management Plan would include the Cost Management Plan, the Cost Baseline and Performance Measurement Baseline.

Project Funding Requirements would consist of projected expenditures plus anticipated liabilities.

Examples of Organisational Process Assets include; existing formal and informal cost control-related policies, procedures, and guidelines, cost control tools and the monitoring and reporting methods to be used.

Tools and Techniques

Amongst the tools and techniques recommended for cost management planning are the following, Expert Judgement, Data Analytics and Project Management Information Systems.

Expert Judgement, using expert knowledge and insight into forecasting, financing and variance analysis

Data Analysis Various data analysis techniques can be used to monitor and maintain costs, such as the following:

Earned Value Management: Earned Value Management (EVM) is a well-known project management tool that uses information on cost, schedule and work performance to establish the status of a project. By means of a few simple rates, it allows the manager to extrapolate current trends to predict their likely final effect (Czarnigowska, 2008). EVM develops and monitors the following three key dimensions for each work package and control account (PMBOK, 2017). Planned value (PV) which is the authorised budget assigned to scheduled work but not including management reserve. Earned value (EV) is a measure of work performed expressed in terms of the budget authorised for that work. It is the budget associated with the authorised work that has been completed. Actual cost (AC) is the realised cost incurred for the work performed on an activity during a specific time period. It is the total cost incurred in accomplishing the work that the EV measured.

Trend analysis: An examination of project performance over time to determine if performance is improving or deteriorating.

Reserve analysis. Observing the status of contingency and management reserves for the project to determine if they are sufficient or still required.

Project Management Information Systems (PMIS). Often used to monitor the three EVM dimensions (PV, EV, and AC). Light et al (2005) outline how research by Gartner within the IT industry discovered that 75% of projects that use some form of PMIS are more likely to succeed.

Outputs

Some of the outputs would include

Project Management Plan Updates, which would include changes to the Cost Management Plan and Cost Baseline.

Project Document Updates, which would include updates to the following: Assumptions Log, Risk Register, Cost Estimates and Basis of Estimates.

Cost Forecasts:, such as a calculated EAC value or a bottom-up EAC value which is documented and communicated to stakeholders.

Change Requests, which are processed for review and disposition through the Perform Integrated Change Control process.